Everything you need to know to navigate the financial institution insurance market in ≈ 5 minutes per week. Delivered on Fridays.

4 claims advocacy lessons from recovering $250M in claims for clients

|

Reading time: 6 minutes Welcome to the Pride, If used correctly, your claim’s advocate can be worth more than your policy limit. But almost all companies underutilize them. In this edition, we will share our lessons learned from recovering over $250 million in claims recoveries for clients through the right advocacy. We’ll cover:

This isn't your typical white paper. This is a no-BS, battle-tested guide to improving your recovery conditions - even if your carrier says they can’t help you.

What is claims advocacy, and why does it matter?During his second year as a broker, one of our Managing Partners, Mark “Flip” Flippen, had an investment fund client hit with an informal SEC inquiry. It turned into a full investigation and eventual lawsuit. A few things were eye-opening:

Claims advocacy is the process of supporting and defending your company when someone files a legal claim against it. Basically: When plaintiffs file a claim against you, who steps up to the plate to fight for your interests? If insurance is like a shield that protects you from harm, claims advocacy is the sword that fights on your behalf when trouble strikes. Everything we do as insurance brokers is to prepare our clients for claims. If you google “what matters for claims advocacy”, it’ll tell you:

But this misses the most important variable in claims advocacy. While many financial institutions assume that coverage is the be-all and end-all; however, our decades in the trenches have shown, there's a factor that's even more critical: Choosing the right carrier.

Is your institution protected when it matters most?Picture this: Plaintiff attorneys hit your institution with a claim. You think you're covered. After all, you negotiated full coverage, so you HAVE to be covered, right? Well yes, but actually, no. What most insurance brokers don’t tell their clients is that you can get coverage right a thousand percent of the time. Finding the right coverage isn’t hard. Finding the right carrier, however, is another story. If you work with the wrong carrier, if you’re not careful, they’ll try to bleed you out with time. Here’s the horror scenario we’ve seen a dozen times:

Having the wrong broker makes this even worse. When your carrier is slow to respond, it’s up to your broker to have your back and negotiate hard with the insurer in this scenario.

Battling with a claim is hard. Battling with a claim and insurer simultaneously is hell.The fallout of a claims dispute can be catastrophic. You're left dealing not just the claim itself, but an insurer with deep pockets and a team of lawyers trained to wear you down. The financial and emotional strain can be immense. Again, we learned this firsthand. In another claim, Flip & Tash handled a complex professional liability matter for an insurance company client. They had potential coverage from their reinsurance tower and commercial market policies, but it was unclear which applied first. The lack of clarity around which should pay first led to carriers fighting the LION team tooth and nail. If you have an unfair insurance carrier during a claim, they will make your life hell for 3 to 5 years. So what can you do about it?

LION’s 4-step blueprint to claims advocacy (from 4 decades of experience)How much money can you possibly make from changing your claim’s advocate? Let us answer that question with a story - The biggest claim Flip ever worked on was a professional liability claim for a bank client. “We took it over from another broker, who’d convinced them $55M was the best offer they'd get from the panel of carriers. But we weren't satisfied with that. Over a couple of months, we leveraged our longstanding carrier relationships to negotiate an additional $500,000 from the lead carrier. That set off a cascading effect, which ended up adding an extra $15M in additional recovery for our client.” As you can tell, the difference between a good and an exceptional claims advocate is massive. In this case, an extra $15 million! See, negotiating claims isn’t about pounding the table - It’s an art that requires you to pull different levers, most of which require trust built over YEARS in the market. After nearly three decades in the insurance space, we’ve done this several dozen times. Here’s our process for ensuring our clients get the right coverage from the right carrier every time: 1. Vet Your Carrier's Claims HandlingBefore you sign on the dotted line, you need to know how your carrier behaves when a claim hits. Here are the main 4 things to look for:

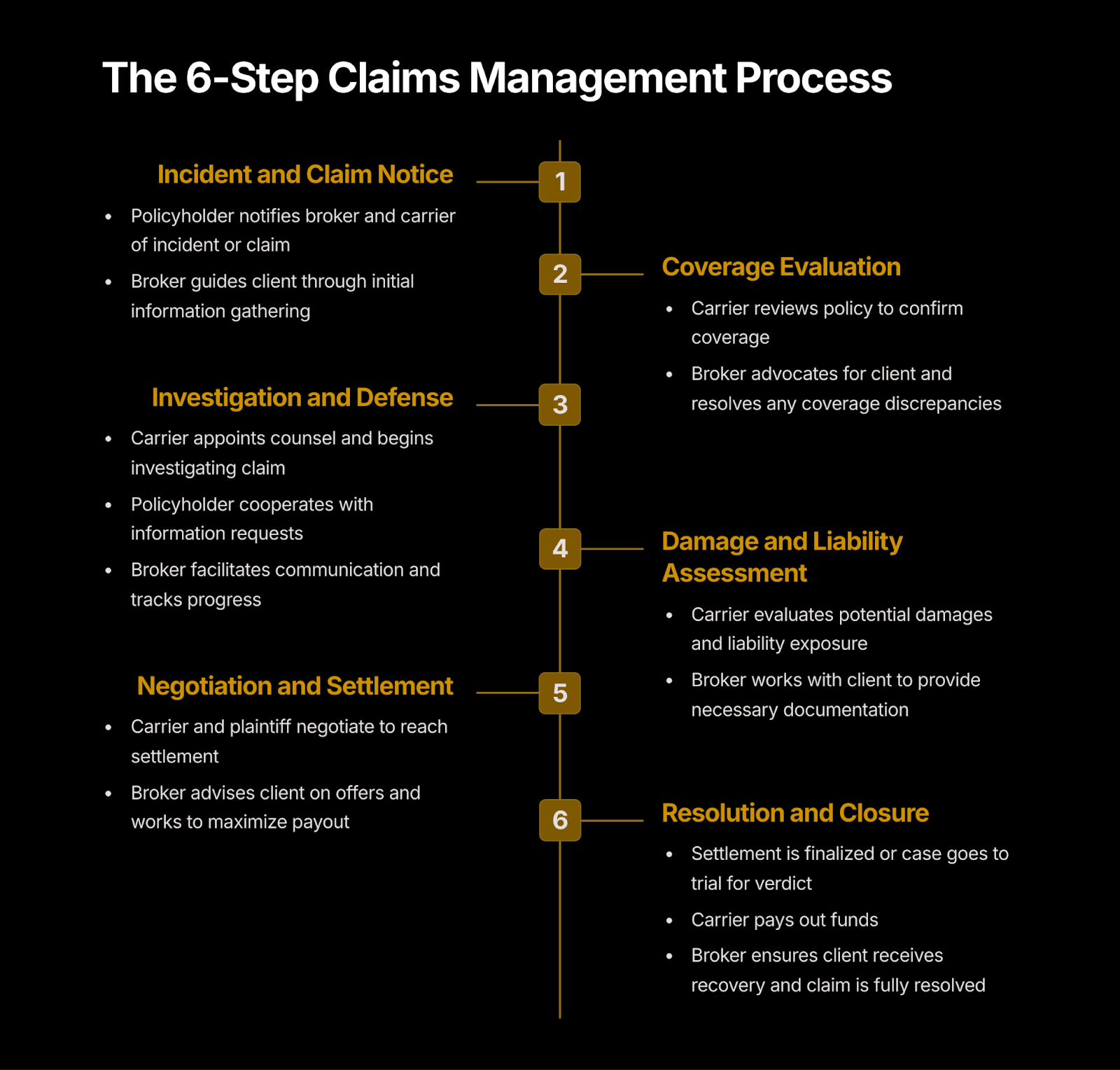

2. Insist on Crystal-Clear CoverageWith the right carrier secured, the next step is ironing out your coverage. This means: • Understanding your unique risks inside and out • Crafting policy language that leaves no room for interpretation • Aligning all parties on the intent behind every clause Think of it like constructing a building. You wouldn't wait for a hurricane to find out if your foundation is solid. You'd insist on the best materials and workmanship from day one. Claims readiness works the same way - the groundwork you lay in advance determines how you weather the storm. 3. Understand the Claims Management ProcessHere’s a high-level overview of what a claims management process looks like:

We’ve spent decades helping clients navigate over $250M in claims scenarios. Our playbook is built on real-world experience and proven strategies, designed to help you recover faster, more effectively, and with less hassle. Next Wednesday’s edition will break down our exact 10-step playbook. (If you got forwarded this email, subscribe to the LION newsletter here to get it in your inbox) 4. Work with an experienced broker that does step 1 and 2 for youTo tell if your broker knows their carriers inside out, ask them 3 questions:

If your broker answers these with a 10/10 confidence level, you’re good. If not, it’s a huge red flag. Your broker might be handing you with their B-team. If your institution works with a mega broker and spends less than $7 million on insurance a year, that’s likely the case. We know because we worked for mega brokers ourselves - smaller clients were underserved. At LION, we've handled hundreds of claims with dozens of carriers. We know exactly how each one operates. When we recommend a carrier, it's based on hard data about their claims track record. (Learn more about us here)

Want to share this edition via text, social media, or email? Just copy and paste this link: lionspecialty.ck.page/posts/4-claims-advocacy-lessons-from-recovering-250m-in-claims-for-clients We get it - this stuff can be overwhelming. That's why we're here - to be your guides and advocates. If you're unsure about your current claims readiness, we'd love to chat. We'll review your carrier lineup and policies, and give you our honest take on where you stand. Contact us here On Wednesdays, we’ll send you an actionable newsletter like this breaking down 1 fundamental in insurance. It’s our “Financial Institution Insurance Fundamentals” series. We’d love to hear your feedback on this 1st edition - Did we succeed in making it an interesting read? Do you want even deeper details? Shorter? Longer? Stay covered, Natasha & Mark Co-Founders and Managing Partners Lion Specialty |

LION Specialty

Everything you need to know to navigate the financial institution insurance market in ≈ 5 minutes per week. Delivered on Fridays.

Reading scan time: 5 minutesListening time: 8 mins Your Friday Five Every week our team rips through 200+ insurance, legal, and market-risk articles so you don't have to! Three developments caught our attention this week: Over 100 C-suite insurance leaders now rank AI adverse outcomes as their #1 long-term emerging risk ahead of climate, armed conflict, and demographic shifts. The migration from geopolitical to technological risk is accelerating. The U.S. Treasury announced meetings with...

Reading time: 4 minutes A line-by-line audit of your Silent AI exposure This week we're launching a three-part Wednesday Intelligence series called The Six-Line Silent AI Audit. It maps the core policy lines in your financial institution's program against the AI exposures the forms were never written to address. Part 1 covers D&O and EPLI, where "wrongful act" definitions assume a human made the decision and algorithmic discrimination doesn't map to your form's coverage trigger. Part 2 covers...

Reading scan time: 5 minutesListening time: 8 mins Your Friday Five This week we're doing something slightly different. One topic, "Silent A.I." Three articles. All on the single most consequential coverage development facing financial institutions in 2026. Most boards haven't been fully briefed on it until now! AI-related lawsuits surged 978% from 2021 to 2025. Most of the policies covering those defendants never mention the word "AI." Silent AI coverage is disappearing from your program...